Life insurance guidefor expats in Spain

Taking out life insurance is a sound financial decision and an act of love and responsibility toward the people you love most.

This guide covers everything English-speaking residents and expats in Spain need to know: the types of cover available, how much capital to insure, how Spanish inheritance law interacts with your policy, where to buy, and how pricing actually works. Written by Life5 Legal, regulated by DGSFP License J3945, policies underwritten by AXA Aurora Vida (DGSFP C0711).

- Backed by AXA

- 100% English process

- Regulated by DGSFP

The right insurance for your personal situation

Life insurance adapts to all kinds of situations. A few examples of how it fits the lives of expats in Spain.

Types of life insurance

Understanding your own needs and goals — and those of the people you want to protect — is the first step to picking the right policy.

Who should I name as beneficiary?

Your children

Whether you're a single parent, widowed, or married with kids — protect their daily expenses, education, and the lifestyle you've built together. The payout can cover years of school fees, university, and the adjustment your family will need.

Your partner

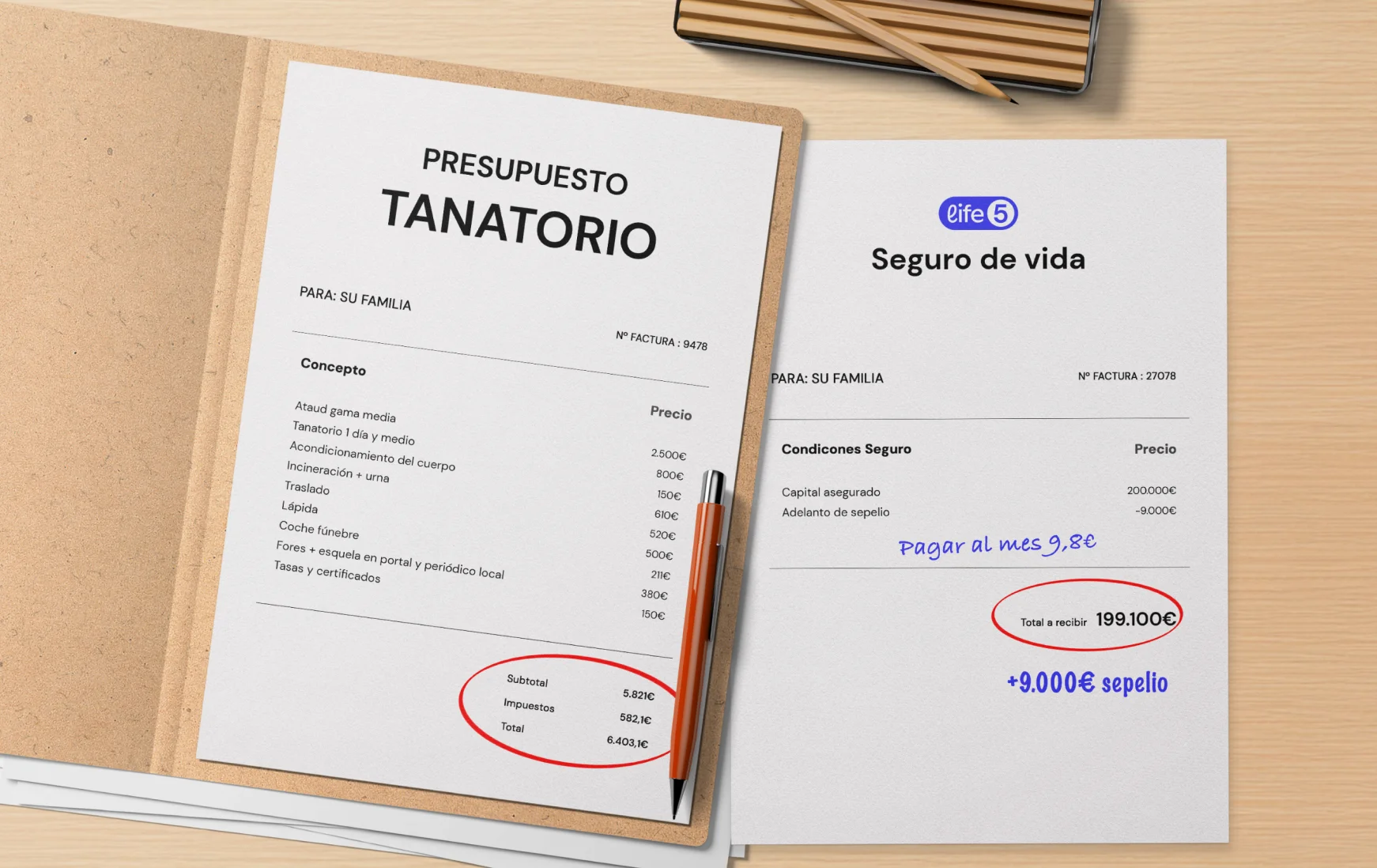

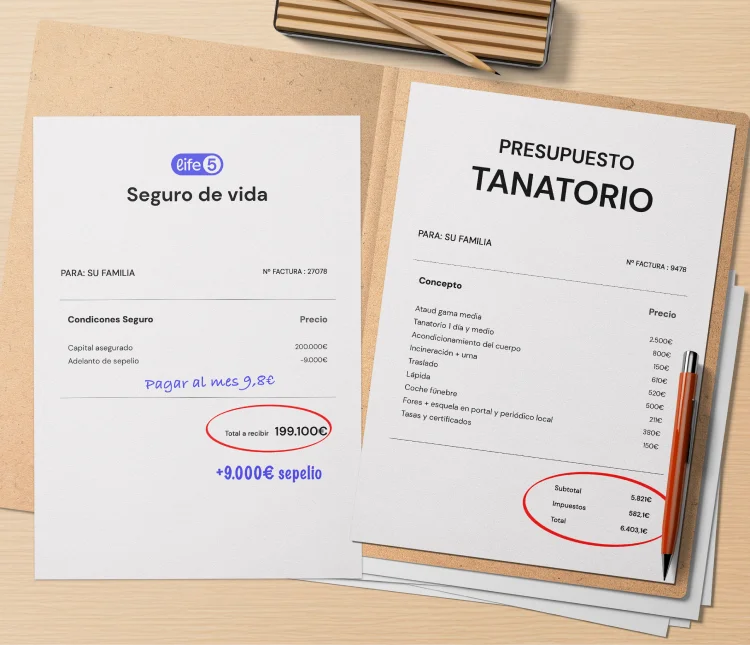

Don't leave your spouse or partner with financial worries — the house, the mortgage, the car, the kids. The payout can also help cover the Spanish Inheritance Tax (ISD) so they don't have to sell assets to pay the tax bill.

Your future

The Total Permanent Disability (TPD) rider pays you directly if an illness or accident permanently prevents you from working — financial support for the life-changing costs that come with disability.

Your parents or dependent relatives

If your parents depend on you financially — common for expats supporting family back home — the death benefit can fund elderly care (Spanish residencias run €2,000/mo+) or repatriation to their home country.

Other causes

Pets? You can name a trusted person and allocate part of the payout for their care. Charities? Many of our customers name NGOs (in Spain or their home country) as partial beneficiaries. The choice is 100% yours — Spanish inheritance law does not restrict it.

Life insurance or seguro de decesos?

47% of people in Spain have a seguro de decesos (funeral-only insurance). It's a Spain-specific product most expats haven't heard of — and usually a standard life insurance policy is a better deal.

In a Spanish inheritance, you can't simply leave everything to the person you choose — Spanish law (Código Civil) divides estates into 3 parts:

-

33.3% Legítima (forced heirship): reserved for heirs the law designates (typically children, then spouse, then parents).

-

33.3% Mejora ("enhancement"): you pick how to distribute this portion among the legítima heirs (e.g., favor one child over another).

-

33.3% Libre disposición (free disposition): entirely your choice — anyone, including non-family.

Key expat insight: your Life5 life insurance payout is NOT part of the inheritance. 100% of the beneficiary designation is yours — you allocate it however you want (spouse, children, parents abroad, charity), and Spanish forced-heirship rules do not apply to it. This is one of the biggest reasons expats use life insurance in Spain as a legacy-planning tool independent of the will.

How much capital do I need to insure?

Two questions to start with:

- How much money would you need if an illness or accident prevented you from working and your income stopped?

- How much would your family need to maintain their standard of living if you were no longer there?

Below, four typical scenarios for expats in Spain. These figures are illustrative averages — our advisors model the exact number for your situation in a 15-minute call.

Family with dependent children

- Raising and educating a child in Spain can cost up to €300,000.

- Outstanding mortgage or other debts: around €100,000.

- Financial cushion for spouse: €40,000.

- Funeral expenses: €6,000.

- Spanish Inheritance Tax (ISD): €4,000 (varies hugely by region — Madrid has 99% bonificación).

Daily expenses: food, transport, clothing, childcare and education.

Total: €450,000

"Spanish widow's pension covers 52-70% of the regulatory base. Orphan's pension covers only a percentage up to a certain age."

"Permanent Disability pension also covers only a percentage of your salary. The new situation typically creates additional expenses."

Couple without children

- Outstanding mortgage or other debts: €100,000.

- Financial cushion for partner: €40,000.

- Funeral expenses: €6,000.

- Spanish Inheritance Tax (ISD): €4,000.

Daily expenses: around €600/mo excluding housing (rent or mortgage). ~€50,000 (varies by household).

Total: €200,000

Where can I buy life insurance in Spain?

Insurers / Agents

Buying directly from traditional insurance companies takes longer. They usually require more paperwork and carry higher prices — lots of bureaucracy, often Spanish-only.

Comparators

A reasonable option to compare prices and guarantees across insurers, but it's one more step in the chain. Some offer discounts; most aren't specialized in life insurance specifically.

Brokers (corredurías)

Licensed insurance brokers work for the client — they can recommend the best insurer for you and carry products from multiple companies. Many of them distribute Life5's products.

Life5

We're a tech-first insurance broker specialized in life cover, regulated by DGSFP license J3945, with policies underwritten by AXA Aurora Vida. Online signup in minutes (via health questionnaire) or by phone. Fair price, personalized advice, 100% in English — built for expats in Spain.

I want my life insurance with Life5

Great decision. Here are the steps — easy, fully online, 100% in English. Built for expats who'd rather not wrestle with Spanish bureaucracy.

What's your risk profile?

To assess risk and calculate your premium, insurers look at:

1. Age. You can sign up between ages 18 and 74 and stay covered up to age 80. Older age = higher risk = higher premium.

2. Profession and risk activities. Some jobs and hobbies carry higher risk. At Life5 we cover even motorcyclists of any engine size — unusual in the Spanish market.

3. Lifestyle. Non-smoking or regular exercise can help you get better terms.

4. Health. At Life5 we insure people with 700+ medical conditions. The severity of each case influences eligibility and premium.

5. Capital and riders. Higher coverage = higher premium. TPD and critical illness riders add to the base price.

How the premium is calculated

Age is one of the primary factors in life insurance pricing. The calculation is based on mortality statistics published by Spain's National Statistics Institute (INE).

For example, in 2022 the probability of death for a 40-year-old was 0.00074%. For €100,000 of insured capital, the estimated premium would be about €74/year.

These tables show general data, but each person has a unique risk profile based on health, lifestyle, and profession. That's why insurers use health questionnaires to fine-tune the premium fairly and individually. The initial quote may adjust slightly after final underwriting, since the premium depends directly on individual risk.

Documents you receive when signing (Legal Notice & Policy)

These 4 steps confirm you as insured. Documents in English and Spanish — the Spanish version is the legally binding one per DGSFP requirements.

"Always answer the health questionnaire truthfully. If the insurer discovers misrepresentation, they may refuse to pay the claim — Spanish law (Art. 10 Ley de Contrato de Seguro 50/1980) treats undisclosed facts as dolo (willful concealment), which can void the policy entirely."

Questions or need help?

Life5 cuenta con expertos en seguros de vida que te ayudarán con el proceso y contestarán todas tus preguntas acerca del seguro de vida.

By email

Send us an email at ayuda@life5.com with your name, DNI/NIE, and a short summary of your question. We reply in under 12 hours, in English.

By phone

Call us free at +34 911 984 986, Mon–Fri 9:00–19:30 CET. English-speaking advisors available.